02 02 2022 | by Victor Xing | Capital Markets

All articles 6

08 26 2019 | by Victor Xing | Economics

Prolonged stimulus paves way for wealth redistribution

05 20 2018 | by Victor Xing | Central Banks

Alternative narrative on the natural rate of interest

01 07 2018 | by Victor Xing | Capital Markets

Flatter yield curve a symptom of ineffective tightening

12 04 2017 | by Victor Xing | Central Banks

Bond market term premium and wolves of Yellowstone

09 20 2017 | by Victor Xing | Central Banks

QE’s distributional effects a rising political liability

09 20 2017 | by Victor Xing | Central Banks

QE’s distributional effects a rising political liability

[The below article was published on Financial Times on September 19, 2017; please visit this link]

Executive Summary

- Officials from major central banks have previously acknowledged QE’s distributional effects but expected aggregate economic benefits of these unconventional policies to outweigh their costs

- Post-crisis asset price appreciation became well entrenched under the effect of QE, which out-paced median wage growth to unintentionally burden low-to-middle income households and individuals with limited asset ownership

- Rising inequality in-turn fueled discontent and contributed to the rise of anti-establishment political candidates

- Efforts by elected officials to ease the effects of policy-induced inequality would likely bolster support toward further redistribution policies such as “helicopter money” to threaten central bank monetary policy independence

- Some prudent officials are taking action: along with Claudio Borio from the Bank of International Settlements, Chief Executive Chan of the Hong Kong Monetary Authority recently highlighted unconventional policies’ distributional effects and urged research into rising inequality’s economic, social, and political impacts

Mechanisms of unconventional policy easing and its distributional effects

Monetary policies rely on financial markets as a medium to affect the real economy (this is at the core of central banks’ focus on financial conditions), and unconventional policies such as quantitative easing (QE) are no exception. Some of the mechanisms and objectives behind QE are as follows:

- Central bank would use newly created digital ledger entries (a.k.a. “money printing”) to buy long-maturity bonds in the open market and push down long-term interest rates (bond yields decline as prices rise)

- Borrowing costs correlated with long-term interest rates (such as mortgage rates and corporate borrowing cost) would decline and incentivize individuals and corporate borrowers to pull forward future expenditure

- By depressing safe haven investment returns (such as Treasury securities), risk adverse investors would be pushed to invest in riskier sectors such stocks, corporate high yield borrowing (credit risk), and real asset (liquidity risk)

In essence, QE facilitates credit easing by incentivizing re-leveraging and utilizes a “recruitment channel” to induce private sector market participants (the “transmission mechanism”) to help monetary authorities depress long-term interest rates and push up risk asset valuation (this will play a key role in this discussion, more on this later). Policymakers have acknowledged monetary policies’ distributional effects on several occasions, but such effects are generally tolerated for as long as the overall effects are expected to help achieve policy mandates. Boston Fed President Rosengren highlighted some of these distributional effects during a 2016 Q&A session and explained FOMC’s decision to keep rates low:

“There are distributional effects that occur with monetary policy. When we lower interest rates, there are definitely some people worse off. The people that are worse off are people that are saving. But the people that are better off are the people who are borrowing. So take my daughter, who is in medical school, with student loans, and wants to buy a house, wants to buy a car, wants to buy new clothes, and then look at how many houses, cars and new clothes you [savers] are looking to buy.

“So you are affected by the fact of low interest rates, but your consumption pattern probably won’t be dramatically affected as her consumption pattern. What that means is that when I am trying to get a good effect for the overall economy, the people who are borrowing tend to do more consumption than the people who are saving. And as a result, lower interest rates do tend to result in a stronger economy than we otherwise would have.”

Absence of wage growth magnified QE’s distributional effects

President Rosengren and other policymakers generally projected that wage growth would materialize in due time (although Governor Brainard have expressed concerns). Its continued absence amid QE’s persistent push in elevating asset prices begin to foster an unexpected turn of events in parts of the country outside of economic hubs:

- Monetary policies that depend on financial markets as a transmission medium would inevitably concentrate its effects on asset prices (asset price inflation, with housing costs being one manifestation of this effect)

- Individuals with limited asset ownership would have to rely on “trickle-down” effects to benefit from QE programs

- Lower borrowing costs would incentivize consumers and business entities to borrow and spend, thus motivating other businesses to expand and push up hiring to create jobs for asset-less individuals

- “Trickle-down” benefits relies on a sequence of assumptions based on well-research policy frameworks; as long as the framework produces the expected result, all are expected to benefit from QE (even though entities with asset and capital would still enjoy greater benefits than those relying on wage growth)

Amongst these policy frameworks, Phillips curve (decline in unemployment would push up inflation via wage pressure) is generally considered the bedrock of modern inflation policies. In their analysis, policymakers assumed that rising wages from higher employment would help low to middle-income households keep up with policy-induced asset price inflation, and the income and wealth gaps between asset owners and the asset-less would thus be kept in check.

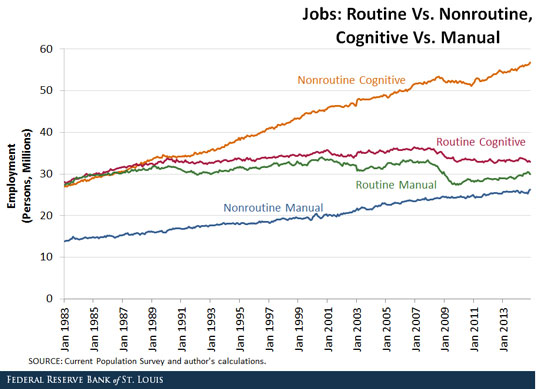

Unfortunately, broad-based wage growth did not manifest as projected by models. St. Louis Fed researchers attributed this to effects of job polarization as technology improvements and a globalized work force steadily dampened demands for middle-skill (and middle-income) jobs that perform routine functions, and New York Fed researchers also recognized the declines in real median wage amongst low-to-middle skill workers that reflect declines in labor pricing power:

Employment recovery in routine and manual jobs lagged behind non-routine cognitive fields:

Thus, as asset price appreciation become entrenched well ahead of wage growth, those who experienced stagnant pay became further burdened by effects of QE

- Young workers facing disappointing employment prospects in rural America came to face a new dilemma: rapid rises in housing costs made living near economic hubs unaffordable

- The time-honored U.S. labor force dynamism and “move with the jobs” spirit could not overcome rising rental and housing prices; the lack of affordable housing also turned would-be buyers into “involuntary renters” to compete against young renters for affordable housing

Policymakers are taking note of these developments, and Minneapolis Fed President Kashkari recently retweeted a WSJ report highlighting workers outside of economic hubs had little choice but to remain where they were, as (QE induced) asset price appreciation in major metropolitan regions created additional and unexpected barriers of entry.

The political consequence of policy-induced inequality

Inequality issues are generally outside of monetary authorities’ policy purview (although Chair Yellen had outlined her low rates policy in terms of her desire to help middle and lower-income families), for they are largely responsibilities of elected officials and fiscal authorities. However, social discontent (partly due to distributional expansionary monetary policy) have already generated political (hence economic) outcomes in the form of Brexit and rise of anti-establishment movements:

- Dissatisfied voters in regions experiencing economic hardship lost faith in establishment political candidates, for their optimism on the economy did not resonate with voters who continued to experience acute hardship

- Voters in parts rural America, the working poor inside economic hubs with trouble scraping together $400 to pay for emergency expenses after housing bills, as well as U.K. pensioners facing lower fixed income returns and higher cost of living had reasons to view establishment policies with skepticism

- With few able to distinguish the roles of elected officials (legislators and fiscal authorities) from monetary officials, the former took the blunt of voter dissatisfaction and became casualties under the wave of populist rebellion

Acknowledging the shift in political tide, U.K. PM May’s remarks in her post-Brexit referendum speech was unsurprising:

“But today, too many people in positions of power behave as though they have more in common with international elites than with the people down the road, the people they employ, the people they pass in the street.”

“But if you believe you’re a citizen of the world, you’re a citizen of nowhere. You don’t understand what the very word ‘citizenship’ means.”

PM May also acknowledged QE’s “bad effects” to contradict Bank of England Governor Carney’s effort to keep rates low:

“Because while monetary policy – with super-low interest rates and quantitative easing – provided the necessary emergency medicine after the financial crash, we have to acknowledge there have been some bad side effects.”

“People with assets have got richer. People without them have suffered. People with mortgages have found their debts cheaper. People with savings have found themselves poorer.”

“A change has got to come. And we are going to deliver it. Because that’s what a Conservative Government can do.”

Once elected officials recognize QE’s distributional effects that exacerbated inequality amid uneven wage growth, thus fueling populist support toward unconventional political challengers, their well-honed self-preservation instincts would likely redirect the object of voter dissatisfaction toward another convenient target: central bank officials and their “irresponsible monetary adventurism.”

This would offer an effective segue to allow establishment candidates to tap into populist support and morph their candidacy away from traditional partisan issues (which are vulnerable to disruptors) into struggles for those disadvantaged by distributional central bank policies (which was featured prominently in PM May’s speech).

These views can be seen in Jeremy Corbyn’s push toward “People’s QE” as well as recent discussions over Universal Basic Income via debt monetization, which is based on Milton Friedman’s “Helicopter Money” to bypass financial sector in the transmission of ultra-accommodative monetary policies, i.e. “channel QE money directly to the people and communities!”

- Jeremy Corbyn’s “People’s Quantitative Easing” works as follows:

- BOE would print money (via digital ledger entries similar to traditional QE) to either directly buy HM Treasury’s debt issuance, or directly transfer money to Treasury to pay for government expenditure

- Government projects funded by “People’s QE” will enhance worker skill and create job opportunities

- Ben Bernanke’s essay on Milton Friedman’s “Helicopter Money” highlighted mechanisms of debt-monetization

- The Fed would print money to pay for the increase in Federal expenditure

- Higher government spending will directly send cash rebates to individuals or fund fiscal programs

Needless to say, both of these proposals would infringe on central banks’ hard-won monetary policy independence (by turning them into on-demand cash machines for fiscal authorities), and it would be difficult for monetary authorities to terminate debt-financed fiscal expansion after it was set in motion (social pressure would make an exit politically difficult, for opponents to debt monetization would be labeled as “opponents to making QE fair again”).

The subjugation of monetary policy independence would quickly manifest in rapid rise of inflation (as seen after the Federal Reserve ceded monetary policy control to the Treasury to monetizing war expenditure during WWII). Memories of events leading to the 1951 Treasury-Federal Reserve Accord had largely faded overtime, and some are again viewing extraordinary monetary policy tools as more persistent fixtures in the real economy. Fiscal authorities in control of monetary policies would be incentivized to maintain reflationary effects and “kick the can down the road” so subsequent administrations would face the difficult task of tightening monetary policy to counter inflationary pressure.

Distributional effects of unconventional monetary policy is not costless to monetary authorities, for central bank monetary policy independence would be at risk if elected officials turn to counter the distributional effects with further economic distortion.

Hong Kong Monetary Authority’s new focus on QE’s distributional effects

Chief Executive Chan of the Hong Kong Monetary Authority (HKMA) made the following concluding remarks at the Jackson Hole Economic Symposium, marking this one of the few occasions when central bank officials highlighted distributional effects of unconventional monetary policy (the other prominent official being Claudio Borio, head of Monetary and Economic Department at Bank of International Settlements):

- There needs to be more research and study by economists, central bankers and policymakers on the distributional effects of unconventional policy

- Policymakers need to understand more on the trend of rising income and wealth inequality and its economic, social and political impact

- Policymakers also need to study more on the labor displacing impact of technological innovations

- Governments are generally more equipped to tax income but less so in wealth. Policymakers must consider what can and should be done to deal with the rising concentration in the distribution of income and more so wealth. It is also not too early for policymakers to consider what should be done to pre-distribute income by helping those displaced workforce to re-train or adapt to the new environment

HMKA’s focus on QE’s distributional effects should be perceived as an early indicator on growing awareness by prudent policymakers. As financial instability risks morph into political risks to impact elected officials, unconventional monetary policies and their distributional effects would likely be treated as a political liability rather than economic asset.

Disclaimer: not investment advice.